IPO Insights: Tips for Successful SEC Staff Review of Your IPO

Last updated October 2, 2023

8 minute read |

The IPO process is lengthy and the review of the IPO by the SEC’s Division of Corporation Finance (“Corp. Fin.”) is a time-consuming part of the process. Corp. Fin. reviews a company’s registration statement to ensure compliance with SEC disclosure rules and federal securities laws, and to ensure the disclosure provided to investors is clear, balanced and not misleading. The typical timeframe for SEC review is between 90 to 150 days. Below, we shed some light on the SEC Staff’s IPO review process and offer tips for effectively managing it.

The general policy is for the Staff to do a “full review” every IPO. This means your IPO will be assigned to a legal and accounting team at the SEC who are primarily responsible for the review. Each review team consists of four members, comprised of a legal examiner (junior attorney) and a legal reviewer (senior attorney), and an accounting examiner (junior accountant) and an accounting reviewer (senior accountant). Although the SEC review team has primary responsibility for the IPO review, the teams may also consult with other offices at the SEC regarding any novel or complex issues.

The following tips and guidance should help to ensure that the SEC review process runs as smoothly as possible.

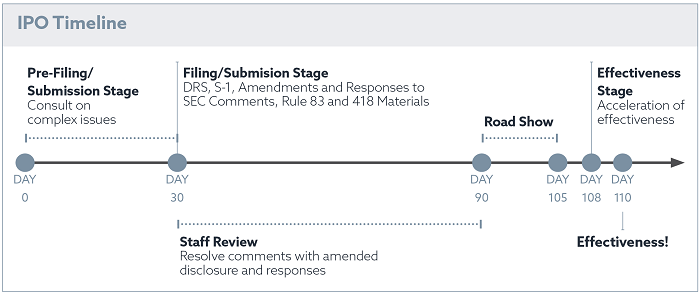

Pre-Filing/Submission Stage

Tip 1

You should contact the SEC to advise them on a pre-filing basis if you anticipate any novel, thorny, or complex issues with your IPO. For instance, in preparing for an IPO, your attorneys or auditors may see issues that are not easily addressed by precedent. Consulting with certain offices within the SEC, such as CF-OCA (Corp. Fin.’s Office of Chief Accountant), may help resolve accounting issues, like seeking a waiver, on a pre-filing basis.

Tip 2

You should consider initially “submitting” your registration statement as a confidential Draft Registration Statement (“DRS”). DRSs are submitted and not technically “filed.” A DRS submission means the registration statement and the Staff’s review is confidential and the public cannot view the registration statement until the company “files” the public registration statement (sometimes referred to as “flipping public”). Amendments to the DRS can be submitted to the SEC confidentially, as well as responses to SEC comments. DRSs will ultimately be available for public review once you flip public. If you decide not to proceed with your IPO, you may retract your DRS to preserve confidentiality by submitting a letter to the Staff requesting to do so.

Tip 3

You can request confidential treatment of certain information otherwise required to be disclosed in the registration statement under Exchange Act Rule 24b-2 and Securities Act Rule 406 if the disclosure of information may result in competitive harm or adversely affect the company’s business and financial position. Most often such requests relate to information that would otherwise be included in exhibits to the registration statement. You should also prepared to submit supplemental materials in connection with the confidential information under the SEC’s FOIA Rule 83 and Rule 418 under the Securities Act if requested by the SEC. Protection under these rules is predicated on requesting the confidentiality at the same time as the submission, which may also include providing back-up for factual statements or claims made in the registration statement or to provide further explanations to the Staff. The Staff may not request the supplemental materials but has the discretion to do so. Rule 83 affords your materials confidential protection while in the possession of the Staff and Rule 418 allows you to request return of the materials or destruction of the materials.

Filing/Submission Stage

Tip 4

You should expect a written comment letter on your initial filing/submission within 27 to 30 calendar days from filing. Generally, your legal examiner will call and inform you that the SEC is reviewing the initial filing within about 10 calendar days. If you do not hear from the Staff after 10 calendar days, you should feel free to call Corp. Fin., which can be found on the SEC webpage. Corp. Fin. monitors the main telephone number and should respond promptly to your call.

After you amend your DRS or public filing in response to the initial round of SEC comments, you should expect to hear a response from the Staff within 14 to 16 calendar days from the date of the amendment. Generally, it is not advisable to follow-up with the Staff until the 14 to 16 calendar day period is completed or you are close to effectiveness and have resolved material comments. The Staff maintains a dashboard of all filings and amendments and works expeditiously to respond. Calling to check on the status only slows down the process. However, if you do not hear from the Staff after this period, feel free to call any member of your review team.

You should be aware that all correspondence to the Staff and correspondence from the Staff will be released publicly after you go effective. Generally, if you retract your DRS or withdraw your registration statement, correspondence is not released.

Tip 5

Feel free to call all members of the legal and accounting teams who are listed on the comment letter if you have any questions or wish to discuss the comments received. It is not necessary to funnel your contact through the legal examiner even though he or she may be your primary contact and you can reach out to the accounting examiner and reviewer in connection with any accounting related questions.

Generally, the first comment letter will be the longest and contain most of the material issues. Subsequent letters should be shorter and each round should resolve the material issues through disclosure or discussions with the Staff. If material issues remain, it is a good idea to request a conference call to understand the Staff’s views better and to avoid extra back and forth.

In this regard, phone calls to clarify comments or seek further guidance are welcomed by the Staff. However, discussions on materiality or applicability of comments should always be formalized in writing. Similarly, the Staff normally does not pre-clear responses to comments on the phone and always considers the written response to be the official response.

Tip 6

You should carefully consider the commencement of your road show because you must file your registration statement publicly—exit the confidential DRS process—15 calendar days before commencing the road show. The road show is important for timing the market window for your IPO. The day of filing your public registration statement is considered Day 1 and you can begin your road show on Day 16.

Tip 7

You should advise the Staff of the timing of your road show and filing of the red herring prospectus (the prospectus that includes a price range) as you whittle down the comments and material issues with your IPO. It is a good idea to give the Staff notice as early as possible. The Staff is generally amenable and will coordinate to help you meet your reasonable expectations. The best practice is to resolve all the material issues before commencing the road show to avoid having to re-file and re-distribute the registration statement during the road show.

Tip 8

As above, you should advise the Staff as early as possible of your timing to go effective. A company should request effectiveness 48 hours prior to the time of effectiveness. The Staff at times may be amenable to an accelerated time frame, but it is not preferable. Every Associate Director (“AD”) who declares a registration statement effective must make a public interest finding in connection with the filing. This means an AD may ask for further clarification or raise an issue right before effectiveness. It is good practice to ask the Staff to see if the AD will start their review earlier rather than later in the effectiveness process so no surprise issues arise at the last minute.

Effectiveness Stage

Tip 9

Your legal examiner will call to advise that the registration statement is effective. You should notify them as soon as possible if you do not want to go effective or delay effectiveness. The SEC no longer issues paper orders. All orders are electronic and posted publicly on EDGAR very early in the morning the day after effectiveness. You may check your order online. You should also check for return of your supplemental materials if you have requested their return.

For more information, visit Orrick’s “Are You IPO Ready?” resource center.